Published March 12, 2026

Seller Financing: The Powerful Real Estate Strategy Many Homeowners Overlook

Seller Financing: What Homeowners and Buyers Should Know

In today’s real estate market, traditional mortgage financing isn’t always the best or easiest path for every buyer or seller. Higher interest rates, stricter lending requirements, and increased loan costs have caused many people to explore alternative strategies. One option that has gained renewed attention is seller financing. Seller financing can create opportunities for both parties when structured properly. It allows buyers to access more favorable terms while giving sellers the ability to potentially earn additional income and achieve a higher sales price. However, like any financial arrangement, it comes with important risks and considerations. Understanding the full picture can help homeowners and buyers determine whether seller financing is a smart option for their situation.

What Exactly Is Seller Financing?

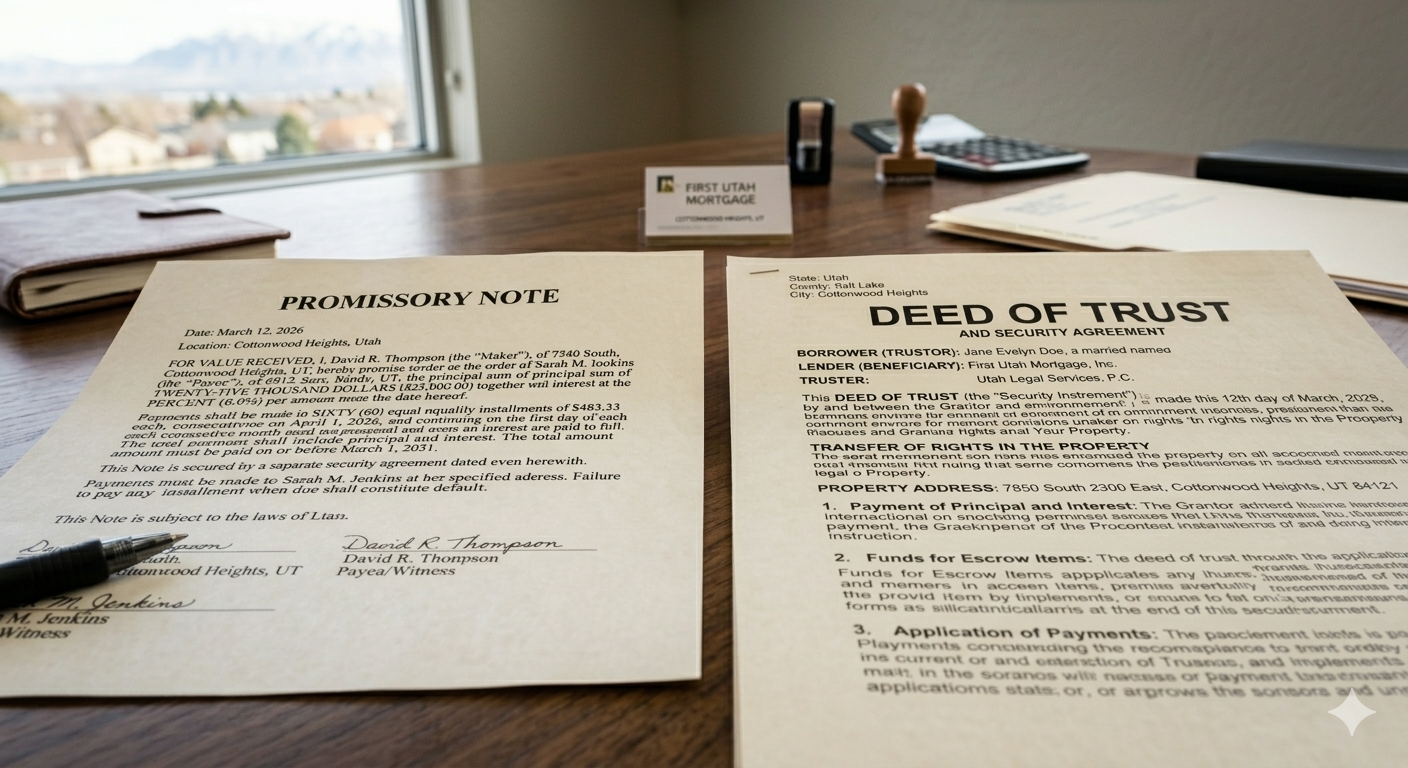

Seller financing, sometimes referred to as owner financing, occurs when the seller of a property acts as the lender for the buyer. Instead of the buyer obtaining a loan from a traditional bank or mortgage company, the seller allows the buyer to make payments directly to them over time. The terms of the loan including interest rate, payment schedule, and duration are negotiated between the buyer and seller. Typically, the buyer provides a down payment, and the remaining balance is financed through a promissory note, which is secured by a deed of trust recorded against the property.

Why Seller Financing Can Be Attractive for Buyers

For buyers, seller financing can open doors that traditional lenders sometimes close. A seller may be able to offer terms that are more flexible and appealing than those available through banks. In many cases, buyers benefit from:

Lower interest rates

Sellers may offer interest rates below current market mortgage rates to attract buyers or justify a higher purchase price.

Flexible loan structures

Some agreements may include interest-only payments, shorter loan terms, or balloon payments that give buyers time to refinance later.

Lower loan acquisition costs

Traditional mortgages often come with appraisal fees, underwriting fees, origination charges, and other closing costs. Often times Seller financing can reduce and even remove these expenses.

Simplified qualification requirements

Banks often require strict income documentation, credit thresholds, and debt ratios. Sellers may be more flexible when evaluating a buyer’s financial profile. In some cases, a buyer may be financially responsible and capable, but their financial structure simply does not fit within the rigid qualification standards used by traditional lenders. For buyers who are self-employed, rebuilding credit, or simply looking for creative financing, this can make homeownership more attainable.

Potential Benefits for Sellers

Seller financing is not just a buyer advantage. In many cases, sellers can benefit financially and strategically from offering financing.

Potential for a higher sales price

When sellers offer attractive financing terms such as a lower interest rate or flexible payments, they often increase the pool of interested buyers. This expanded demand can allow the property to command a higher price.

Interest income

Instead of receiving the entire sale price at closing, sellers effectively become the lender. That means they collect interest payments over time, which can significantly increase the total amount received from the transaction.

Structured tax advantages

For sellers who are not completing a 1031 exchange, seller financing can provide a way to spread capital gains across multiple years through an installment sale structure. Rather than recognizing the entire gain in one tax year, income may be distributed over the life of the loan.

Regular income stream

Seller financing can function almost like a retirement income strategy. Monthly payments from the buyer can provide consistent cash flow over time.

Risks and Concerns Sellers Should Consider

While seller financing can be beneficial, it is not without risk. One of the biggest concerns sellers face is buyer default.

Questions sellers should consider include:

- How financially stable is the buyer?

- Will the buyer honor the agreed payment terms?

- What happens if the buyer stops paying?

If a buyer defaults, the seller may need to pursue foreclosure or other legal remedies to reclaim the property. Another concern involves property conditions. If a buyer fails to maintain the home and the seller eventually takes it back, the property could be returned in worse condition than when it was sold. Because of these risks, sellers should carefully evaluate buyers and ensure the agreement is structured properly with legal protections.

Existing Mortgages Can Complicate Seller Financing

Seller financing may also be limited when a property still has an existing mortgage. Many mortgages contain due-on-sale clauses, which allow the lender to demand full repayment if ownership transfers. If the seller carries financing while still having an underlying loan, the buyer could technically be in a junior position behind the original lender. Some buyers are uncomfortable with this structure, and it should always be reviewed carefully with legal and financial professionals. Most buyers today are only comfortable doing a seller finance deal with a homeowner if there are no underlying mortgages recorded on the property.

Is Seller Financing Right for Everyone?

Seller financing can be an excellent tool, but it is not appropriate for every transaction. Some sellers simply need the full proceeds from the sale immediately. Others may not be comfortable acting as a lender or managing the risk associated with buyer payments. Similarly, some buyers prefer the stability of traditional financing or may not want to navigate a more customized agreement. However, when both parties understand the structure and protections involved, seller financing can create win-win outcomes that might not be possible through traditional lending alone.

Final Thoughts

Seller financing is one of the more creative tools available in real estate. When structured carefully, it can help buyers secure favorable terms while allowing sellers to potentially increase their sale price and generate long-term income. The key is understanding the benefits, risks, and legal considerations before moving forward. Real estate is rarely one-size-fits-all. Sometimes the right structure simply requires looking at the transaction from a different angle.

If you’re considering selling your home and want to explore whether seller financing might be a viable strategy, it’s worth having a thoughtful conversation with our team at Lemonade Real Estate to learn about how it could fit into your overall goals.